Medical debt can sneak up fast—and feel impossible to escape. One unexpected injury or illness can bury you in bills, even without insurance. But there’s hope.

These 15 proven strategies can help you crush medical debt before it crushes you. Whether you’re just getting started or already overwhelmed, there’s a smart next step you can take right now.

1. Ask for an Itemized Bill

Medical bills often have errors. Ask for a detailed list of charges to check for duplicates, incorrect services, or overcharges.

2. Negotiate Before You Pay

Call the billing office and try to negotiate. Many providers will reduce charges if you cannot afford the full amount.

3. Apply for Financial Assistance

Nonprofit hospitals are required to offer charity care programs. Fill out the paperwork—they may forgive a big part of your bill.

4. Set Up a Payment Plan

Most hospitals offer interest-free payment plans. These plans allow you to spread the debt to pay it off without draining your budget.

5. Look Into Medical Credit Cards with Caution

Some providers push special credit cards. These can help—but only if you pay them off before high interest. Read the fine print carefully.

6. Check Your Insurance Coverage

Make sure your provider billed your insurance correctly. Follow up on claims, denials, or missing payments to avoid being charged twice.

7. Use an HSA or FSA if You Have One

You can use Health Savings Accounts and Flexible Spending Accounts to pay medical bills with pre-tax dollars.

8. Get Help from a Medical Billing Advocate

Billing advocates specialize in spotting errors, negotiating prices, and navigating insurance claims. Some work on a sliding scale—or even for free.

9. Prioritize High-Interest Debts

If you used credit cards or loans to cover medical bills, tackle those balances first. Interest can grow faster than the original debt.

10. Avoid Paying with High-Interest Credit Cards

If possible, don’t put medical debt on a credit card. It turns manageable bills into high-interest trouble.

11. Know Your Rights Under the No Surprises Act

Since 2022, federal law has protected you from surprise out-of-network charges for emergency care and specific scheduled procedures. If you receive an unfair medical bill, you can use these protections to dispute it.

12. Don’t Ignore Collection Notices

Ignoring debt won’t make it go away. Contact the collector, verify the debt, and negotiate a payment plan or settlement.

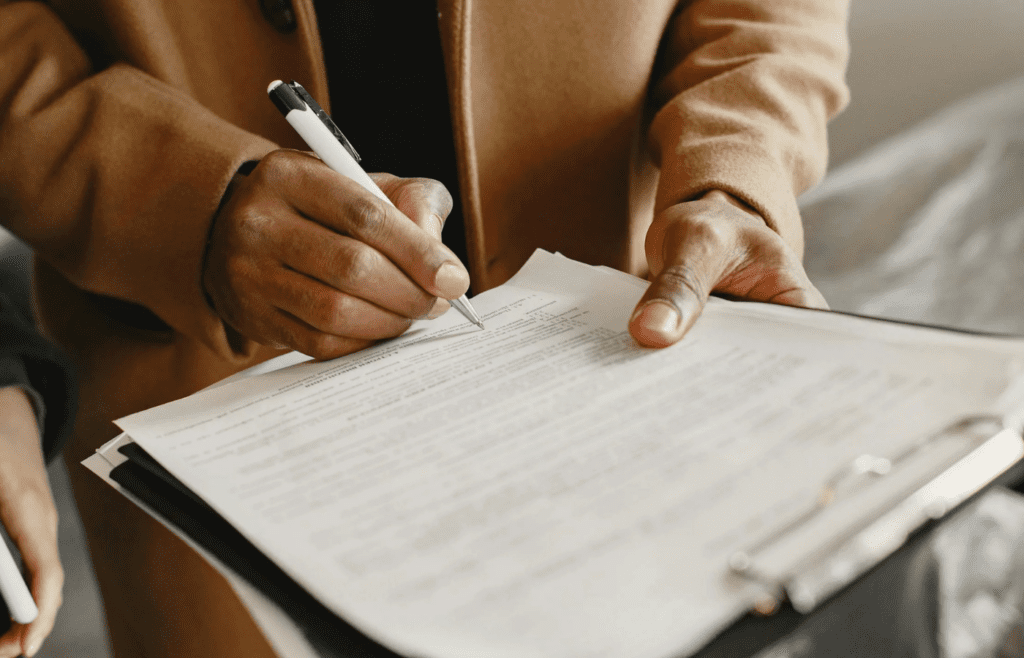

13. Get the Agreement in Writing

If you settle or agree on a payment plan, always get it in writing. Protect yourself with proof of the deal.

Read More: 10 Uncomfortable Truths About Personal Debt Management

14. Avoid Taking on More Medical Debt Without a Plan

Ask about costs upfront when possible. If you need treatment, work with providers to estimate bills and explore aid before the procedure.

Read More: 15 Essential Tips to Survive Rising Debt

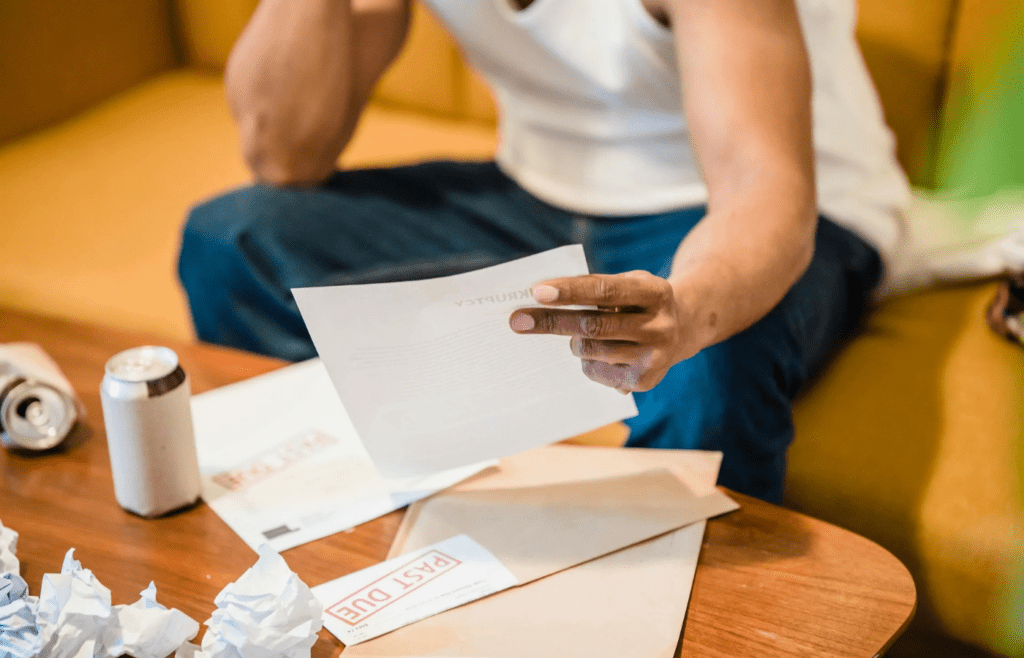

15. Consider Bankruptcy Only as a Last Resort

Medical debt is a common reason people file—but it’s not a quick fix. Talk to a credit counselor first to find another way out.

Medical debt feels personal—but you don’t have to fight it alone. With persistence, planning, and the proper support, you can regain control and protect your financial future.

Read More: 20 Ways to Save Money on Healthcare